Did You Know?

We serve loans, the best way you can borrow

Borrowing money should be simple, safe and stress-free. But some terms in loan agreements can confuse people. One of those is indemnity. Suppose a lender asks you to sign an indemnity clause. It means you are agreeing to cover losses or damages.

Knowing what it means will save you from any trouble. Here, you will learn what indemnity really is, how it works, and why understanding it matters when applying for loans.

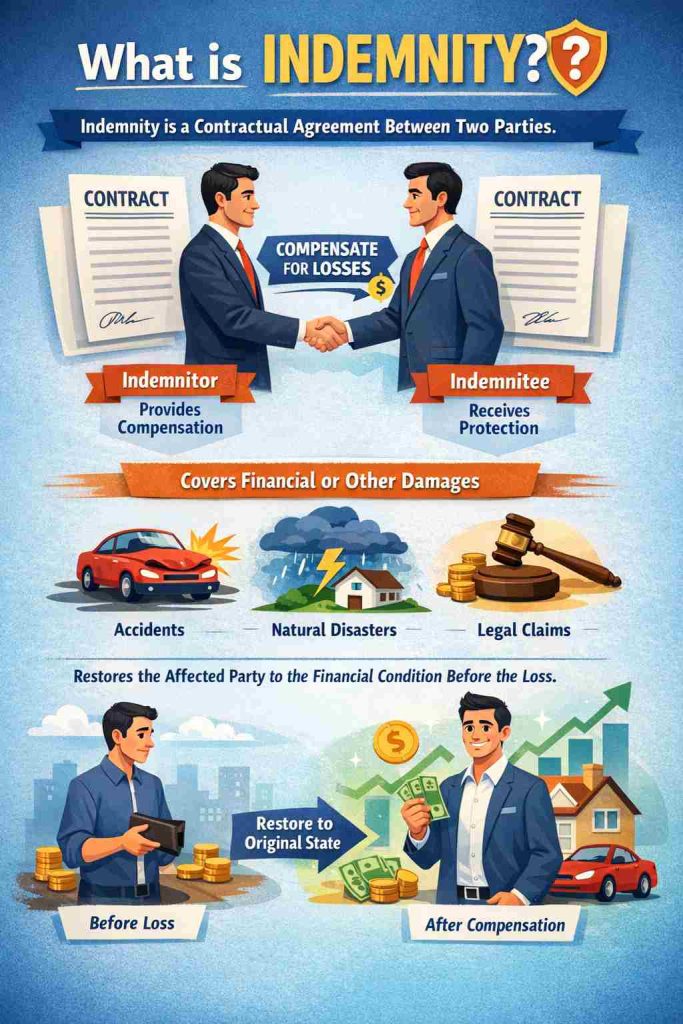

What is Indemnity? Simply put, it is a contractual agreement between two parties. One party compensates another for financial or any other damages due to certain events. It helps restore the affected party to the financial condition before the loss or damage.

Indemnity has been around for more than a century. Here are a few things to learn about its history –

1. In the Bygone Days - In old times, winning kingdoms made the losers pay significant indemnity sums, often in gold. This helped the winners grow stronger in money and power.

2. In Medieval Europe - In Europe, local rulers gave indemnity to merchants for safety. It helped protect them from attacks, thefts, and unexpected trouble during travel.

3. Insurance Development - India saw the start of insurance in 1818 with the Oriental Life Insurance Company in Calcutta. Later, the British Insurance Act and the Bombay Mutual Life Assurance Society followed.

4. Legal and Contractual Framework - In 1912, India passed a law to manage life insurance. LIC began in 1956. IRDAI was formed in 2000 to manage insurance rules.

5. Modern Indemnity Practices - Today, indemnity is used in many fields like insurance, construction, and services. It helps avoid money loss and keeps deals fair.

Indemnity insurance pays for losses caused by a person's work, accident, or service. The insurer promises to pay the affected party. You may have to pay a premium, and when a loss happens, the insurer handles it based on the policy. It is used often in legal, medical and business sectors.

There are many kinds of indemnity, each with a different use. Let's understand the most common ones.

1. Contractual Indemnity - This is when two people agree in writing that one will pay for losses. It is written in legal contracts to share risk.

2. Insurance Indemnity - This is when one compensates for the damage or loss of another. If misfortune happens, the insurer will pay the cost.

3. Statutory Indemnity - This comes from government rules. Some laws force businesses to offer indemnity to staff or customers under certain conditions.

4. Cross Indemnity - This happens when both (or multiple) parties agree to protect each other from losses. It is used in large agreements or joint ventures (like service agreements, real estate transactions, etc.).

5. Self Indemnity - In this case, people keep money aside to cover losses on their own instead of depending on insurance.

Indemnity can change how your personal loan works. It adds safety for the lender but may also create more steps for you.

1. Reduces the risk of lending

2. Prevents financial loss

3. Ensures actions against protection due to unnatural scenarios

4. Helps with complicated loan steps

5. Prevents security interests

When you borrow money, both sides want safety. That is where indemnity plays an important role in lending and borrowing.

1. Reducing Risks - It lowers the risk lenders face when something goes wrong with a loan or the borrower fails to repay.

2. Protecting - It protects both the borrower & lender from sudden expenses or unexpected legal problems tied to the loan.

3. Legal Liability - It helps manage legal duties. If someone breaks the terms, indemnity helps settle issues without long disputes.

4. Insurance - Some loans are linked with indemnity insurance to add extra cover. It protects from missed payments or damages.

5. Measuring Financial Security - Lenders use indemnity to check if the borrower can handle extra responsibilities during financial stress.

Looking for an indemnity example? These real uses show how one side agrees to pay if a loss happens in a business deal:

1. Contractor Agreement - A company hires a helper firm. The contract of indemnity says the subcontractor or helper will pay if their work causes damage or injury.

2. Product Liability - A company selling goods agrees to cover costs if a product defect hurts someone or causes legal problems.

3. Professional Services - A firm giving advice adds indemnity to the contract. They won't be blamed if their advice leads to a client's loss.

Read Also: How to Write a Loan Application Letter?

| Basis | Indemnity Insurance | Life Insurance |

|---|---|---|

| Purpose | Covers actual losses or claims | Offers a fixed payout on death or maturity |

| Coverage | Only pays for losses proved | Pays once after the insured's death |

| Used By | Doctors, lawyers, and businesses | Families and working individuals |

| Focus | Financial safety for work-related issues | Financial safety for the family |

| Payee | Person or business affected | Family member or nominee |

People often mix up indemnity and guarantee. But both work in different ways in financial agreements.

1. Obligation Type - Indemnity covers a loss directly. Guarantee means someone else will pay if the main person fails.

2. Number of Parties - Indemnity only needs two parties. A guarantee always needs three: lender, borrower and guarantor.

3. Claim Process - In indemnity, the lender can claim the loss directly. In a guarantee, they go to the guarantor after the borrower fails.

4. Legal Force - Indemnity is stronger in law. It does not need the main person to fail first. The guarantee requires it first.

5. Responsibility - The person who gives the indemnity is known as the indemnifier. In guarantee, the third person is called the guarantor.

Read also: Personal Loan Guarantor

Professional indemnity insurance helps if a client says your service caused a mistake or loss. It pays for the cost or damage. It is not like general insurance. It only covers losses caused by advice or work, not physical injury at your place.

Hospital indemnity insurance pays for hospital stays that other plans may not cover. It gives extra support when you are admitted. Some companies use this to help if their workers get hurt during working hours.

A fixed indemnity insurance plan gives a set cash amount for listed medical services. It does not change with hospital bills. The insurer pays an amount for each hospitalisation for each day in the hospital.

Also Read: Personal Loan Eligibility Criteria | Personal Loan Documents Required

Thus, now you know that indemnity helps protect both lenders and borrowers in personal loan deals. It keeps rules clear and risks low. Even in an instant personal loan arrangement, indemnity plays a vital role in ensuring legal clarity. Reading all terms before signing is key. When money is urgent, clear terms give peace. Borrow with care, and stay informed about the rights of indemnity holder.

Indemnity in a personal loan means the borrower agrees to pay for any loss the lender faces due to the loan. This includes legal costs or unpaid dues. It protects the lender. The borrower must read all terms before signing. Not understanding this can lead to stress and unexpected payment requests later.

No. Indemnity covers only the losses clearly mentioned in the agreement. It will not cover personal damage, emotional loss, or any costs outside the loan terms. Borrowers should always ask for a copy. Knowing what is & isn't covered helps avoid confusion or extra pressure later.

People who give advice or offer professional services need professional indemnity insurance. Doctors, lawyers, consultants, and builders are common examples. It protects them from claims if their advice or service causes harm. Without it, they may have to pay for big losses from their own pocket. It adds safety to their work.

Lenders use indemnity clauses to protect against money loss. If a borrower breaks the loan terms or causes any loss, the clause helps recover costs. It lowers the lender's risk. The borrower agrees to pay if something goes wrong. This keeps the loan process safe and clear for both sides.

Indemnity is between two parties. The borrower agrees to pay for any damage or loss. A guarantee adds a third person who pays if the borrower fails. With indemnity, the lender can act directly. With a guarantee, they must wait until the borrower misses a payment. Both serve different safety needs.

The borrower must take care not to break the loan rules. If something goes wrong, they must cover the cost. The clause also expects the borrower to act in good faith. If the lender suffers a loss due to their mistake, they must pay. It's a serious part of the agreement.

Suppose the borrower makes a loss and refuses to pay. In that case, the lender can take legal action. Indemnity makes the borrower responsible. Ignoring this clause may result in court cases or extra legal costs. Reading the terms & asking questions before signing helps avoid this kind of trouble later.

No. Indemnity is not required in each personal loan. It totally depends on the lender's rules as well as the borrower's profile. If the lender feels there is risk, they may include it. Some small loans do not need it. Always check your loan papers to see if this clause is added.

Check what loss it covers, who pays, or how much should be paid. Read the full indemnity line word by word. Ask the lender to explain any complicated terms. Never sign without knowing your duties. See if it adds cost or changes the loan terms. Safe borrowing starts with knowing every rule clearly.

Download our personal loan app to apply for a personal loan. Get up to 2Lakhs* as a personal loan. Download Now!

![]()

Sign into avail a personal loan up to ₹ 2,50,000

Unifinz Capital India Limited is a Non Banking Finance Company (NBFC) registered with the Reserve Bank of India (RBI). lendingplate is the brand name under which the company conducts its lending operations and specialises in meeting customer’s instant financial needs.

RBI CMS

RBI CMS RBI Sachet

RBI Sachet