Did You Know?

We serve loans, the best way you can borrow

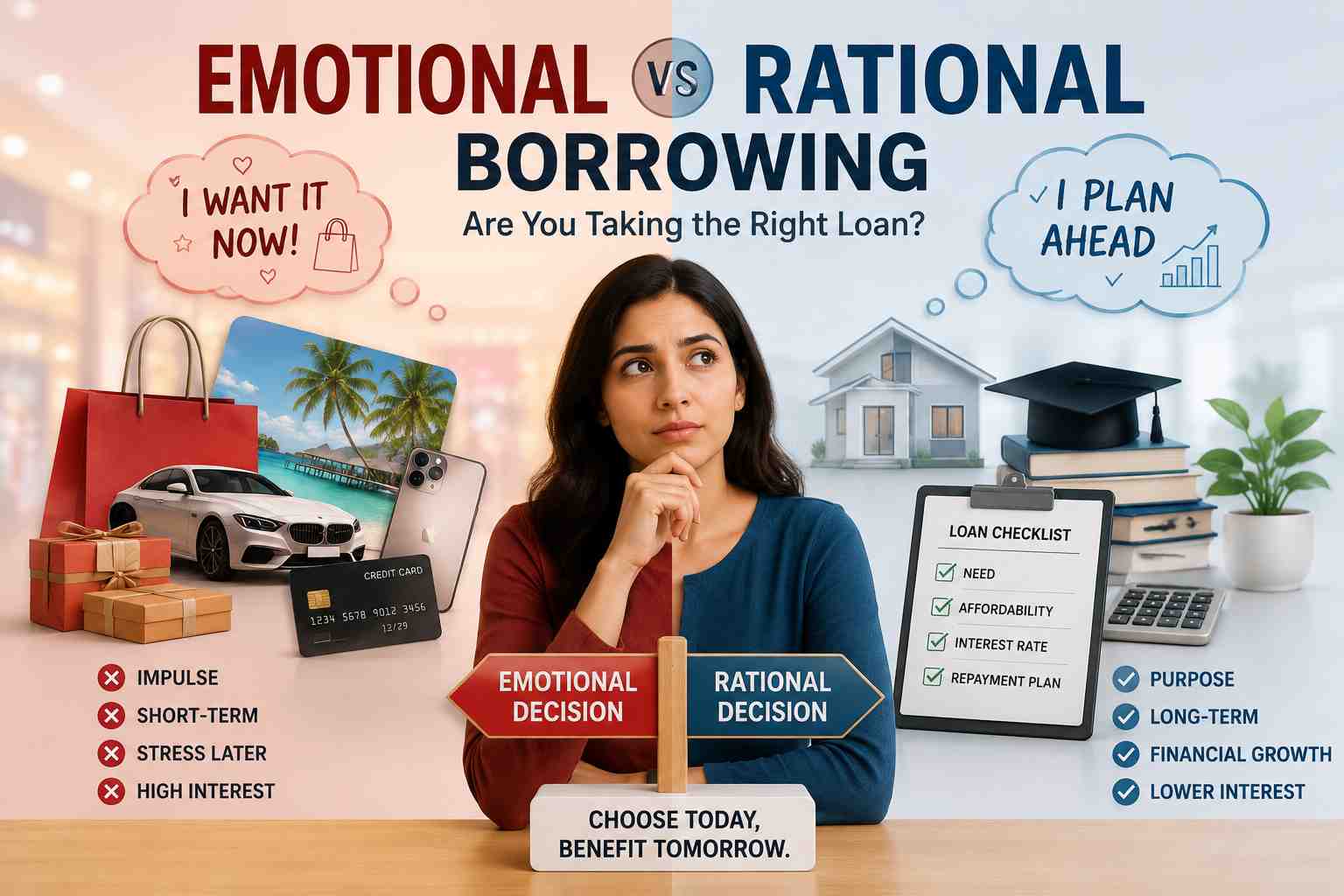

Emotional borrowing happens when you make a decision before thinking anything rationally. You may feel an urge to buy something because of anxiety or social pressure. In such cases, you forget to distinguish between emotional vs rational borrowing. You focus on specific factors that help you feel less anxious. However, you do not think of your repayment plan. It involves impulsive choices in which you overlook the personal loan interest rate because you want the funds immediately. You are prioritising a temporary mood boost over your long-term financial stability & peace of mind.

Rational borrowing is the complete opposite of an impulse buy. It is a structured process where you treat a loan like a strategic tool. When you follow this path, you weigh the necessity of the debt against your current income and future goals. You look at the personal loan eligibility criteria to ensure you actually qualify before applying. This approach requires you to compare different lenders and calculate the total cost of credit. Distinguish between emotional vs rational borrowing to ensure that every rupee borrowed serves a specific purpose in your life.

Here is how emotional vs rational borrowing looks when you compare the core driving factors -

| Parameter | Emotional Borrowing | Rational Borrowing |

|---|---|---|

| Primary Driver | Impulse and feelings | Logic and planning |

| Speed | Instant and rushed | Deliberate and slow |

| Focus | Short-term desire | Long-term impact |

| Research | Little to none | Thorough comparison |

| End Goal | Satisfaction of want | Fulfilment of need |

If you choose emotional vs rational borrowing based on a whim, you might face these specific financial risks.

1. High Interest Costs - When you rush, you often accept a higher personal loan interest rate than necessary. You don't take time to shop around for better deals (which is a big mistake).

2. Debt Traps - Such loans often result in a cycle where you take a new loan to pay off an old one. It results in a debt trap that becomes impossible to repay.

3. Budget Strain - Emotional loans rarely suit your monthly budget. You may find your EMIs eating up cash meant for rent or groceries.

4. Lower Credit Scores - Missing payments because the loan was unaffordable can damage your credit history. That makes it more difficult to get help when you actually need it.

Taking a step back to think logically offers huge advantages for your future self. Here is why rational decisions win every single time.

1. Lower Total Costs - You spend time checking the personal loan processing fee and interest charges. This research ensures you pay the lowest possible amount for the money you use (saving you thousands in the long run).

2. Improved Mental Health - Knowing you can afford your repayments removes the "debt anxiety" that keeps people awake at night. You feel in control because you have a clear, documented plan to clear the balance.

3. Better Financial Habits - Rational borrowing forces you to look at your bank statements. This awareness helps you manage your money better overall, not just when you are applying for an instant personal loan.

Here are the signs that indicate you might be taking a loan on emotional grounds -

1. The Pressure of "Now" - You should pause if you feel a sense of urgency that isn't tied to a real emergency. If you are ignoring the personal loan documents required because you want the cash "now" to satisfy a whim, you are likely acting on pure impulse.

2. Avoidance of Reality - Another sign is when you avoid doing the math because you are afraid of the answer. (We often tell ourselves we "deserve" a treat, but your budget doesn't care about feelings). If you cannot explain the loan's purpose using logic, an instant personal loan might be a mistake.

Moving toward a logical mindset takes a bit of discipline. You can change your habits by following a few simple steps to master emotional vs rational borrowing.

1. Implement a Cooling-Off Period - Wait a minimum of 48 hours before hitting the apply button. This lets us look at the figures with a clear head.

2. Create Needs vs. Wants List - Write down exactly why you need the money. If the reason is a "want" (like a luxury upgrade), consider saving up for it instead of borrowing.

3. Use a Loan Calculator - Physically see the numbers. When you see the total interest you will pay over three years, the "must-have" item often loses its appeal very quickly.

You deserve to have a healthy relationship with debt. Use these practical tips to navigate the world of emotional vs rational borrowing with total confidence.

1. Verify Your Eligibility - Always check personal loan eligibility criteria before you apply. That will prevent unnecessary rejections that can temporarily dip your credit score & cause stress.

2. Read the Fine Print - Don't just look at the monthly EMI. Check for hidden costs like the personal loan processing fee or prepayment penalties that might be buried in the contract.

3. Keep Your Tenure Short - Longer tenures mean lower EMIs. However, they cost more in interest. Aim for the shortest period you can comfortably afford to keep the total cost down.

The choice between emotional vs rational borrowing is about self-awareness. It is okay to want things. However, it is better to afford them. Selecting logic over impulse protects your credit score & your peace of mind. So, you always need to treat a loan as a serious commitment. Take your time & do your research. This way, you can ensure the debt helps your future.

Emotional borrowing is when you take out a loan depending on feelings such as excitement or fear. You may buy something to feel better after a bad day or to keep up with friends. You may ignore the long-term costs of your choice in this state.

The main difference is the "why" and "how" behind the loan. Emotional borrowing is impulsive and focused on immediate desires. Rational borrowing is planned and focuses on financial logic. When you borrow rationally, you compare the personal loan interest rate across lenders and ensure the loan fits into your existing monthly budget.

Most people borrow emotionally because they want instant gratification. The brain's reward system craves the "hit" of a new purchase. Sometimes, it is driven by an "all or nothing" mindset during a perceived crisis. People often forget to look at the personal loan documents required and rush the process to get quick relief.

Guilt, envy, and anxiety are the big ones. You might feel guilty for not providing something for your family or envious of a neighbour's new car. Fear of missing out (FOMO) also plays a huge role. These feelings cloud your judgement and make an instant personal loan seem like a quick fix.

Not always, but it is very risky. Sometimes an emotional impulse leads to a necessary purchase, but the lack of planning usually means you pay more than you should. Without comparing emotional vs rational borrowing pros and cons, you likely end up with a higher interest rate or terms that don't suit you.

Rational borrowing is a logical way to manage debt. It is significant because it helps you avoid overextending your finances. You only take a loan when it makes financial sense & when you have a clear repayment plan. It ensures you meet the personal loan eligibility criteria.

It prevents you from taking on bad debt that may offer no return. Selecting loans with a low personal loan interest rate & manageable EMIs keep your debt to income ratio healthy. It also ensures you can build savings & invest in your future.

You must look at your monthly income, your existing debts, and the total cost of the new loan. Always check the personal loan processing fee and any hidden charges. Ask yourself if the purchase is a necessity and if you can realistically afford the repayments for the entire duration of the loan.

Emotional borrowers usually settle for the first offer they see. This means you often end up with a higher personal loan interest rate because you didn't shop around. Higher interest rates lead to more expensive EMIs, which can lead to a financial crunch (because your budget wasn't prepared for the extra outflow).

Yes, it can. If you take an instant personal loan emotionally and then struggle to pay it back, your credit score will drop. Late payments and defaults stay on your record for years. This makes it much harder for you to get approved for important loans, like a home loan, in the future.

Download our personal loan app to apply for a personal loan. Get up to 2Lakhs* as a personal loan. Download Now!

![]()

Sign into avail a personal loan up to ₹ 2,50,000

Unifinz Capital India Limited is a Non Banking Finance Company (NBFC) registered with the Reserve Bank of India (RBI). lendingplate is the brand name under which the company conducts its lending operations and specialises in meeting customer’s instant financial needs.

RBI CMS

RBI CMS RBI Sachet

RBI Sachet