Did You Know?

We serve loans, the best way you can borrow

When you are shopping for an instant personal loan or taking out a mortgage, the advertised interest rate doesn’t give you a complete view of your total borrowing cost. It merely shows the cost of securing the principal loan sum. However, you should keep in mind that taking out a loan also involves other costs that are not accounted for in the interest rate calculation.

That’s where APR comes into the picture. It is the total annual borrowing cost you pay to take a loan, including interest and associated costs. Read on to understand the difference between APR vs Interest and how it can impact your borrowing decisions.

APR stands for Annual Percentage Rate and encompasses more than the interest rate; it includes any fees and costs associated with getting a loan. The costs may be loan processing fees, broker fees, closing costs and other charges. Unlike the personal loan interest rate, the APR is more effective in determining the total yearly cost of borrowing when comparing loans.

Also Read: What is APR?

An interest rate is the percentage earned or charged on the borrowed amount over time. When you get a loan, the interest rate is used to determine how much one has to pay in addition over a certain period. E.g.: If you take a ₹2,00,000 loan at 8% interest rate, you will owe ₹16,000 in interest after one year.

The rate of interest can be fixed or variable.

1. A fixed interest rate means you will pay a fixed amount (₹16,000 from the above example) throughout the loan term.

2. Variable rate of interest means the interest amount will fluctuate as per the market rates, and so will be your annual interest payments.

A key difference between APR vs Interest Rate is that no fees or charges are included in calculating the latter.

The interest rate is calculated as a percentage of your principal borrowing amount, expressed annually. Below is the formula for interest calculation:

Interest = P x R x T

Here,

P = The principal loan amount, or the amount you borrow.

R = The rate of interest, expressed annually as a percentage of decimal.

T = The number of periods.

Let’s say you have taken out a loan of ₹5,00,000 at an annual interest rate of 8% p.a. for a period of one year. Hence, the total interest amount that you will have to pay on the loan is ₹40,000.

Also read: Factors Affecting Interest Rates

Annual Percentage Rate (APR) isn’t the same as interest rate, but it is the most common measure determining your borrowing cost. However, the only thing that makes personal loan APR vs interest rate different is that the latter does not include all other costs and fees related to taking a loan. Know how to calculate APR:

1. Find the interest rate on your loan from the lender.

2. Indicate any applicable fees or charges on the loan, such as brokerage fees, personal loan processing fees, etc.

3. Account for the principal borrowing amount and interest rate to work out the total interest paid over the loan period.

4. Now, sum the total interest with the total fees or charges.

To understand the difference between APR vs Interest Rate, it’s essential to first comprehend how the Annual Percentage Rate (APR) operates.

The APR is significant because it represents the yearly expense associated with borrowing. This is not just the interest rate, but also all fees or other charges associated with obtaining a loan, so you know really how much that line of credit costs. Your APR is determined based on a review of your creditworthiness by the lender and must be disclosed before you sign the contract. A higher credit score may get you a lower interest rate; however, the associated fees and charges incurred on the loan often remain the same.

The interest rate is the cost of borrowing the principal loan amount, stated by the lender at the time of closing the deal. It can be fixed or variable.

Fixed-interest rate loan — pay a stipulated amount over and above your borrowed principal in this type of loan. The interest payment goes towards paying back towards the principal amount as well as additional money as the cost of borrowing.

In variable-interest rate loans, your rate of interest may vary depending on the market rate set by the Reserve Bank of India.

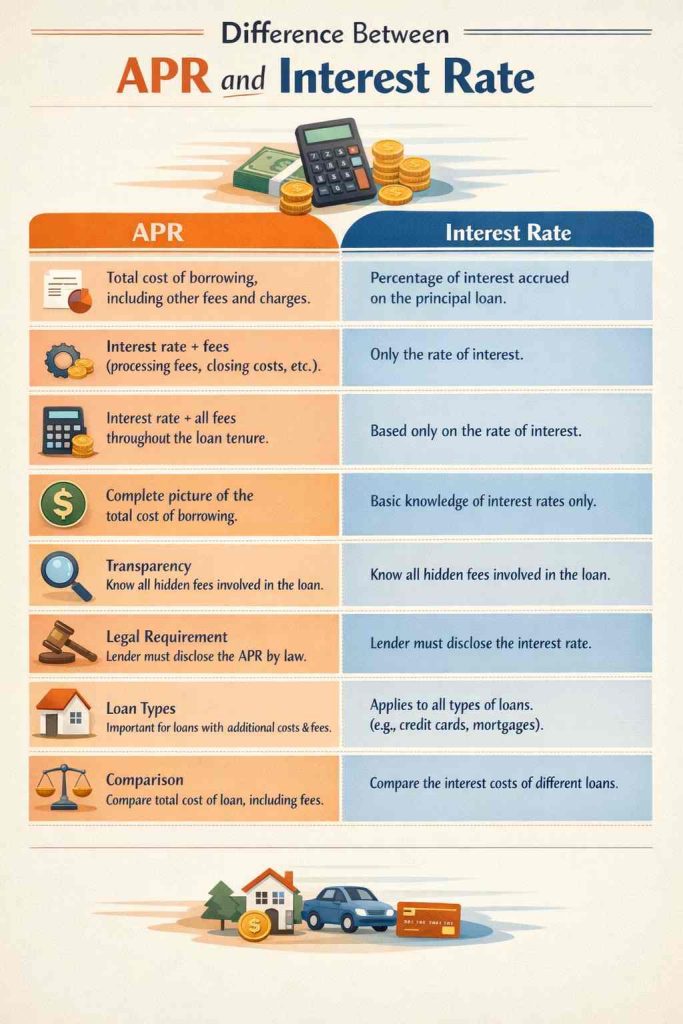

Now, here is a comparison table which can help you understand the prominent differences between APR vs Interest Rate:

| Factors | APR | Interest Rate |

|---|---|---|

| Definition | It is the total cost of borrowing, including other fees and charges. | It is the percentage of interest (fixed or variable) accrued on the principal loan. |

| Components | Rate of interest plus associated charges, such as processing fees, closing costs, etc. | Only the rate of interest. |

| Calculation | APR computation includes the interest rate + all fees you pay throughout the loan tenure. | Interest rate calculation is based only on the rate of interest. |

| Impact on Total Loan Cost | APR gives a complete picture of the total cost of borrowing. | It provides just a basic knowledge of interest rates, not other fees & charges. |

| Transparency | Understanding APR is more comprehensive, and you get to know all the hidden fees applicable to taking out a loan. | How the interest rate accrues on a loan is easier to understand. |

| Legal Requirement | Before you sign the loan proposal, the lender must state the APR as a legal requirement. | The lender is required by law to disclose the interest rate before the deal. |

| Loan Types | APR holds the most importance for loans that involve additional costs and fees. | Interest rate applies to most types of loans, including credit cards, mortgages, personal loans, etc. |

| Comparison | Knowing the APR is crucial for comparing the total cost of a loan, including fees. | It can help you compare the interest costs of different loans. |

Here is an example that will help you understand what is APR vs Interest Rate.

So let us assume you have taken a mortgage of ₹80,00,000 for 30 years at an interest rate of 7.2%.

On the principal is 0.5% as loan processing charges, i.e. ₹40,000.

Using a simple home loan calculation, the total amount (Principal + interest) that you need to pay in 30 years is ₹1,95,49,100.43.

That means you are paying an additional ₹1,15,49,100.43 over and above the principal amount which includes interest amount and additional fees.

So, your APR = ₹6,51,637 (approx.)

Annual interest payment = ₹3,84,970 (approx.)

While the annual interest payment only includes the interest amount you have to pay for borrowing, the APR includes both the interest payment and the additional processing fee.

During the loan tenure, you will need to pay the principal loan amount of ₹80,00,000 + the interest amount + all other costs.

1. Understand APR vs Interest Rate: If you are a person with a long-term financial perspective, compare interest rates. Conversely, if you are interested in receiving the best deal from your monthly repayments, then understanding the APR makes more sense.

2. Check the Lender Terms and Fees: The fees and interest rates associated with a personal loan can add up to your total cost of borrowing. Make the borrower disclose loan terms, including any additional fees.

3. Be Cautious of Loan Duration: Opting for longer loan repayment tenure will reduce your monthly outgo but it also means you would have to pay more in interest over the loan tenure.

Because other fees beyond the rate of interest are included in APR, this is nearly always higher than the interest rate. Processing fees, brokerage fees, closing costs, and other kinds of charges are also factored into APR.

If you prefer a more competitive loan offer with reduced APR rates, check out these tips:

1. Increase Your Credit Score: Having a higher credit score will enable you to get the best APRs. Therefore, take care of lowering the credit utilization ratio, making repayments on time and a lower number of loan enquiries simultaneously.

2. Shop Around: Every lender has a unique interest rate, terms and fee structure. Take APR vs Interest Rate into consideration when deciding how much to borrow and choosing the best financing terms for your situation to pay a lower interest rate plus other charges.

3. Choose a Shorter Loan Term: Choosing a shorter term may lead to lower APR and overall interest payments.

4. Borrow As Little As You Need: Lenders might charge reduced interest costs for small loans, which can help lower your Debt To Income Ratio (DTI).

5. Cut the Best Deal with Lenders: The higher the credit score or the better the bank relationship, more is the legroom to cut better deals in terms of interest rates, fees and APR.

That is all that you need to be aware of about APR vs Interest Rate to compare a wide range of loan offers across multiple lenders. The APR shows total borrowing costs, as opposed to the interest rate, which indicates only the direct borrowing cost. This is because APR also factors in other borrowing costs like additional fees, charges, etc. Knowing how much it will actually cost you to borrow a loan can help you make decisions strategically and sidestep surprise fees.

The APRs are never lower than the interest rates, as the former comprises all fees beyond that of interest. That said, the APR can be equal to the interest rate in loans with no fees.

A 0% APR loan is a loan that does not have interest on the borrowed amount. But borrowers should also be wary because a lot of 0% APR offers are short-term. Meaning, you pay 0% interest for the first six months, with say, 15% APR after that. And 0% APR loans might also come with fees, or money you have to pay up front.

APR vs Interest Rate are similar but have one key difference — the interest rate does not include any fees, which is why APR, combined with it, gives more information about your exact costs. The rate depends on the loan purpose, duration, and other macro-level conditions. You are charged at an APR of 10.45%-12% approximately for taking a personal loan in India.

The interest rate is determined by your credit score, the type of loan, and what the current market conditions are. As a rule of thumb, anything between 10.60% and 16.50% per annum is considered to be quite favourable.

Download our personal loan app to apply for a personal loan. Get up to 2Lakhs* as a personal loan. Download Now!

![]()

Sign into avail a personal loan up to ₹ 2,50,000

Unifinz Capital India Limited is a Non Banking Finance Company (NBFC) registered with the Reserve Bank of India (RBI). lendingplate is the brand name under which the company conducts its lending operations and specialises in meeting customer’s instant financial needs.

RBI CMS

RBI CMS RBI Sachet

RBI Sachet