Did You Know?

We serve loans, the best way you can borrow

The interest coverage ratio helps you work out how many times a company’s earnings can pay its ongoing interest expenses. Lenders and investors decide if a business can take on extra borrowing by looking at the interest coverage ratio.

If the interest coverage ratio is high, it points to a company’s ability to pay interest with ease. A strong interest coverage ratio creates a cushion during short-term dips in earnings. It means debt obligations will continue to be met without too much concern.

So, what is the interest coverage ratio metric? This metric gives you a direct view into how comfortably a company covers its interest payments using its operating earnings. Businesses often rely on borrowings to drive expansion and manage daily operations.

Lenders and investors see stability since regular earnings act as a strong buffer against uncertainty when this number is higher. This makes the metric central for assessing reliability when banks consider lending.

A low interest coverage ratio flags risk. It signals the business could struggle to pay interest if income drops or costs rise unexpectedly. Financial analysts often prefer this ratio above two, with even higher figures indicating a business is comfortably positioned.

Understanding the components of the Interest Coverage Ratio is about seeing if your profits can handle the costs of borrowing. This calculation relies on two numbers—earnings before interest and taxes (EBIT) and the total interest expense.

EBIT is the money left after paying for production and operating costs, but before thinking about loan or tax payments. You find it by subtracting all regular business expenses from your overall revenue, which gives a direct look at your business’s actual performance.

Businesses track EBIT closely because it signals how well daily activities translate into profits, separate from any outside financing. This single number tells if your core tasks, like production or services, leave enough money behind after all the basics are paid. Efficient operations boost EBIT further, helping you set benchmarks and spot ways to boost earnings.

EBIT Formula

EBIT = Revenue – (COGS + Operating Expenses)

Looking at EBIT helps assess liquidity. Your cash flow depends on keeping this number strong, since it must always exceed what you owe in interest.

Interest expenses are the costs from every type of borrowing—bank loans, bonds, and overdrafts included. This figure must account for all payments linked to business debt to make the analysis accurate. Miss one, and the interest coverage ratio will not reflect real risk.

If the interest outflows are large, pressure builds on your working capital and can leave little room for investments. Outside lenders may see you as a risk when the interest coverage ratio formula produces a low result. Consistent reviews of all loans and careful repayment planning help keep ratios healthy.

Also Read: Factors Affecting Interest Rates

| Coverage Ratio | Formula | Purpose |

|---|---|---|

| EBITDA Interest Coverage Ratio | EBITDA ÷ Interest Expense | It checks if earnings before interest as well as amortisation are enough to pay interest. It is useful for businesses that rely on operating cash and want a clear view of repayment ability. |

| EBIT Interest Coverage Ratio | EBIT ÷ Interest Expense | This version uses operating income before tax. It removes depreciation and loan amortisation to focus only on profit from business operations. It is practical when the lender wants to see how well core earnings can manage interest payments. |

| EBITDA Less Capex Interest Coverage Ratio | (EBITDA – Capex) ÷ Interest Expense | This subtracts capital expenses before checking coverage. It fits companies that often spend on equipment or infrastructure and need to show they can still cover interest after essential investments. |

| Fixed Charge Coverage Ratio (FCCR) | (EBITDA – Capex) ÷ (Interest Expense + Current Portion of Long-Term Debt) | The interest coverage ratio meaning adds scheduled debt repayments to interest costs. It shows if earnings are enough to cover fixed payments. |

The interest coverage ratio is calculated using a simple formula:

Interest Coverage Ratio (ICR) = EBIT ÷ Interest Expense, net

Where:

1. EBIT is calculated as Gross Profit minus Operating Expenses

2. Interest Expense, net is the total interest paid minus any interest income received

This formula checks if operating profits are strong enough to cover interest payments without depending on outside support. EBIT is used as the base because it shows income from regular business activity.

Lenders as well as investors use this as a quick check on whether the business can afford its debt costs. It is simple but effective in early-stage credit decisions. The ideal interest coverage ratio depends on industry type and risk appetite, but higher values are usually preferred as they indicate stronger repayment ability.

If not mentioned clearly, this ratio almost always refers to an EBIT-based calculation, since it strikes a balance between strict cash-only metrics and inflated bottom lines.

To understand how to calculate interest coverage ratio, you must divide the operating profit by the interest expense due for the period.

Interest Coverage Ratio = EBIT ÷ Interest Expense

Let’s take a simple example:

Assume that a company has ₹100 crore as EBIT. It pays ₹20 crore in annual interest.

Interest Coverage Ratio = 100 crore ÷ 20 crore = 5.0x

This means the business can pay its current interest five times using its operational earnings. A ratio like this gives lenders confidence that repayments will not be delayed even if earnings drop slightly.

Now imagine if the ratio were just 1.0x. That would mean the company is earning just enough to cover interest. In that case, even a small decline in profit could lead to a missed payment. That’s why this ratio matters so much in early risk assessment.

Analysts look at this number closely while reviewing debt plans. If it’s low, the business usually needs to improve margins or reduce costs before taking on new loans.

Also Read: Fixed and Floating Interest Rates

A company reports revenue of ₹10000000. It records the cost of goods sold at an amount of ₹500000.

The operating expenses of the company include:

1. ₹120000 for salaries

2. ₹500000 for rent

3. ₹200000 for utilities

4. ₹100000 for depreciation

The interest expense during the same period is ₹3000000.

EBIT = Revenue – COGS – Operating Expenses

EBIT = ₹10000000 – ₹500000 – ₹120000 – ₹500000 – ₹200000 – ₹100000 = ₹8680000

Interest Coverage Ratio = ₹8680000 ÷ ₹3000000 = 2.89x

This interest coverage ratio example shows in clear numbers that the company earns almost three times the amount.

The interest coverage ratio tells you straight away if a business can meet its interest payments using money earned from daily operations. Here is what you should know about the importance of the interest coverage ratio.

1. Credit Assessment: Lenders use the interest coverage ratio as it makes the risk of granting loans clear. When this figure is high, there’s evidence that the business is not a risky bet.

2. Investment Evaluation: Investors study the interest coverage ratio to see if payments are manageable long-term. This guides whether they invest or walk away.

3. Strategic Borrowing: Company leaders set borrowing limits using these numbers. This way, businesses avoid taking on more debt than their profits can handle.

4. Risk Detection: When the interest coverage ratio falls, it flashes an immediate warning. It helps teams focus on financial trouble before it becomes unmanageable.

5. Peer Comparison: Comparing this number to competitors' points out if a business is financially sound or needs change.

6. Covenant Fulfilment: Lenders often require a minimum interest coverage ratio as part of loan agreements, so tracking it is about meeting clear, measurable obligations.

The interest coverage ratio shows if a company earns properly from its regular business to pay interest on its loans each time it’s due. This number directly shapes decisions about lending, investment, and expansion. Analysts, lenders, and company managers put their trust in it because it gives a real answer to whether interest payments can actually happen, not just look possible in theory.

1. Lenders and Banks: Use the interest coverage ratio as a filter before approving loans. A lower figure signals higher risk, so approvals slow down if this ratio falls short.

2. Credit Rating Agencies: Focus on this number to help set credit ratings. When a ratio matches or is better than the sector average, companies enjoy borrowing at lower rates.

3. Equity Investors: Use a strong interest coverage ratio to see if a business is stable enough for steady returns and growth.

4. Bond Investors: Rely on it to judge if their payouts will arrive on schedule, shaping every investment choice.

5. Company Management: Track the ratio each quarter to catch early signs that debt might become a threat and tackle problems fast.

6. Financial Analysts: Review it against industry peers and explain what is a good interest coverage ratio is for that area to show real competitive standing.

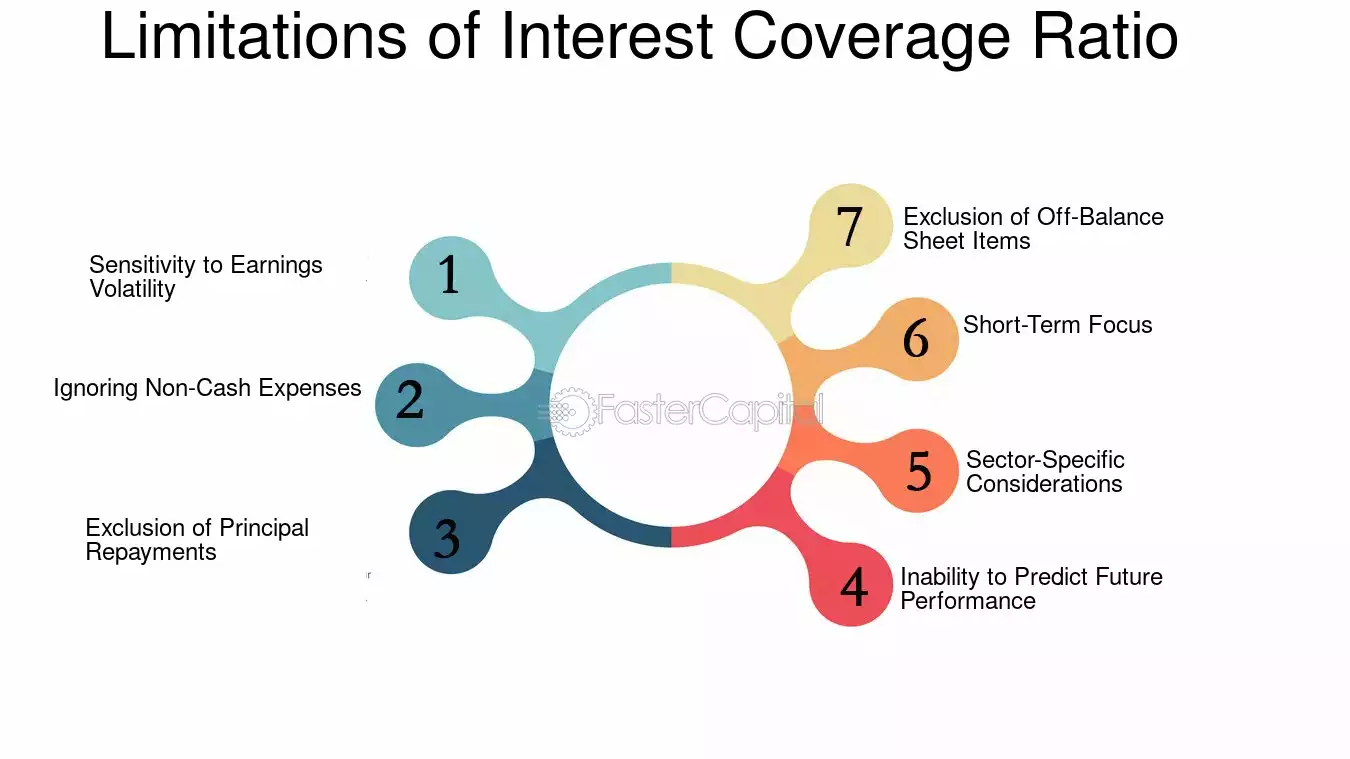

The interest coverage ratio does not give you the whole story if you really want to judge a business’s strength. It skips over repayments on the loan itself and gives you no warning if next year’s profits drop. You cannot rely on it alone, especially when past numbers look good only because of an unusual gain or an accountant’s tricks. The same ratio might mean safety for one sector and trouble for another.

1. Limited Timeframe: This ratio accounts for a single period, so a short burst in profits can make a weak business look more stable than it is.

2. Ignores Principal: You see only the interest payments here. Regular repayments of the loan’s main amount go unnoticed, making risks easy to miss.

3. One-Off Gains: Sometimes, income not related to the usual business boosts the ratio. That makes it hard to see what’s really happening underneath.

4. Relies on Past Profits: Earlier financial results do not always show new challenges, so this ratio might ignore warning signs that start to appear.

5. Sector Variation: Each sector reads this figure differently. A “safe” number in one field can mean a big risk in another.

6. Accounting Choices: Financial statements can be shaped to look stronger than reality, which can make the interest coverage ratio less trustworthy in tough times.

Analysing the interest coverage ratio depicts the ability of a company to meet its debt obligations.

This measure helps lenders as well as investors gauge the reliability of the firm.

1. A ratio below 1 reveals the company struggles to meet its interest payments.

2. A score below 1.5 often indicates potential risk of default or operational weakness.

3. Ratios between 2.5 and 3 signal solid ability to handle existing interest on debt.

4. Higher figures are common in industries prone to unpredictable swings in revenue.

Distinct industry patterns influence what is considered a comfortable coverage ratio, so reference to direct peers matters when drawing comparisons. This metric holds particular importance for those evaluating companies before applying for an instant personal loan.

| Interest Coverage Ratio | Interpretation |

|---|---|

| 1 or less | The business may struggle to meet interest expenses using current earnings, risking financial default. |

| 1.5 to 2 | The business can cover interest payments with earnings but may have limited headroom for downturns. |

| 2 or more | The business stands on firm ground with sufficient earnings to manage interest outgoings comfortably. |

A good interest coverage ratio shows how easily a company manages its debt. Lenders use this to decide if a business handles interest payments, especially as personal loan interest rate factors shift.

1. Higher Leverage Ratio: More debt increases risk. Businesses with higher leverage face greater difficulty meeting their obligations.

2. Higher Interest Coverage Ratio: A higher ratio signals comfortable debt coverage. It reflects stronger financial health and less concern for repayment issues.

Higher ratios always add confidence. Lower ratios reflect risk and reduced borrower reliability.

Interest Coverage Ratio shows a firm’s ability to pay interest alone, while Debt Service Coverage Ratio measures the ability to cover both interest and principal. Both affect the interest rate of your loan.

| Aspect | Interest Coverage Ratio | Debt Service Coverage Ratio |

|---|---|---|

| What it measures | Pay interest only | Pay interest and principal |

| Formula | EBIT ÷ Interest Expenses | Net Operating Income ÷ Debt Service |

| Use case | Quick debt safety check | Complete debt payment analysis |

| Time focus | Current interest obligations | Full loan repayment schedule |

| Risk assessment | Interest payment risk | Overall default risk |

| Calculation complexity | Simple calculation | Requires detailed cash flow data |

| Typical benchmark | Above 2.5 good | Above 1.5 preferred |

| Banker preference | Initial screening | Final loan approval |

| Investor focus | Bond investors | Equity investors |

| Warning signals | Below 1.5 caution | Below 1.0 default risk |

| Industry variation | Varies by sector | More standard across industries |

| Frequency of review | Quarterly or annually | Monthly monitoring |

| What affects it most | Earnings and interest rates | Cash flow and loan structure |

| Best for | Industry comparisons | Loan application evaluation |

The coverage ratio depicts the ability of your earnings to meet ongoing interest payments. The leverage ratio shows the debt funding of assets.

1. Capital Structure: Looks at debt versus equity or total capital, with the debt-to-equity ratio being a prime example for assessing long-term risk.

2. Cash Flow Metrics: Evaluates debt against operating performance, for instance, with debt-to-EBITDA or debt-to-EBIT ratios, showing how business cash flows support obligations.

The interest coverage ratio reflects the ability of a company to meet debt interest payments using its current earnings. It is a strong signal for lenders and investors analysing creditworthiness. When this figure is robust, trust grows around financial health and operational stability, giving insight into future borrowing prospects and decisions regarding sustainable expansion and prudent risk assessment.

The interest coverage ratio is also called “times interest earned.” It shows how many times a company can pay interest before things start getting uncomfortably tight.

This version of the interest coverage ratio uses EBITDA instead of EBIT. It offers a fuller picture by including non-cash expenses that can hide a company's real strength.

A good interest coverage ratio is anything above 3. It means the business isn’t just surviving but has a healthy cushion when things don’t go as planned.

A bad interest coverage ratio falls below 1.5. It tells you the business may be skating on thin ice and cannot afford even a small stumble.

A higher interest coverage ratio is definitely better. It signals peace of mind, with room to breathe when markets wobble or sales drop without warning.

An interest coverage ratio below 1 means the business earns less than what it owes in interest. That’s the financial version of running on empty.

An interest coverage ratio of 1.5 shows the company is hanging on by a thread. There’s little margin for error, and any dip could throw it off balance fast.

The interest coverage ratio turns negative when the company is losing money operationally. That’s a red flag no lender or investor feels good about.

A negative interest coverage ratio means earnings are worse than zero. The company is bleeding money before even paying interest. That’s a tough as well as dangerous position.

Banks check the interest coverage ratio to measure breathing room. Strong ratios build trust, while weak ratios make approvals challenging.

Businesses can raise profits, cut interest costs, and trim wasteful spending to boost the interest coverage ratio.

Download our personal loan app to apply for a personal loan. Get up to 2Lakhs* as a personal loan. Download Now!

![]()

Sign into avail a personal loan up to ₹ 2,50,000

Unifinz Capital India Limited is a Non Banking Finance Company (NBFC) registered with the Reserve Bank of India (RBI). lendingplate is the brand name under which the company conducts its lending operations and specialises in meeting customer’s instant financial needs.

RBI CMS

RBI CMS RBI Sachet

RBI Sachet

{kind=link}