Did You Know?

We serve loans, the best way you can borrow

Searching for a home feels exciting until you face complicated financial calculations that seem confusing. Most first-time homeowners struggle with understanding how much they can borrow against their dream property. The loan to value ratio serves as your financial compass during this challenging time.

Smart borrowers use this ratio to plan their finances better and avoid costly mistakes later. So, how do you explain loan to value ratio?

Key Takeaways

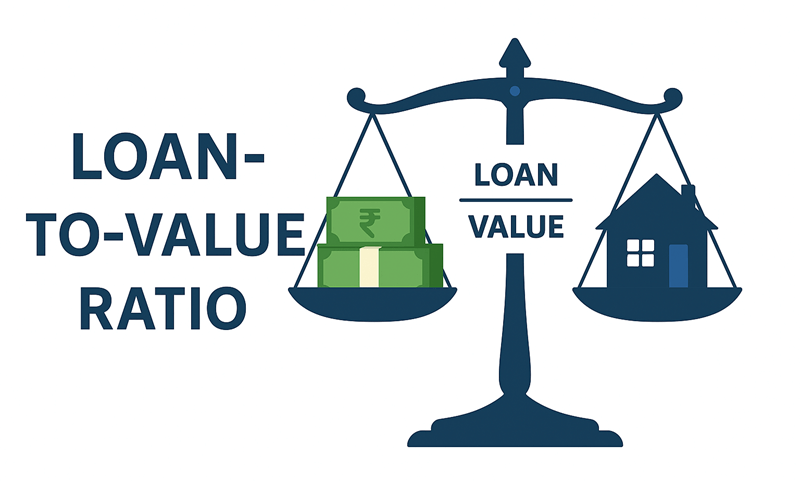

How do you define loan to value ratio? Well, it is the percentage of your property's value you're borrowing from lenders. The lender calculates this ratio to assess the risk when you apply for a home loan. A lower ratio indicates you're putting more money down. That makes lenders feel more comfortable.

Your property is collateral. Thus, lenders wish to ensure they can recover the money easily. The ratio significantly affects your loan terms (including interest rate and approval chances). Higher ratios signal higher risk (lenders become more cautious about lending decisions).

The loan to value ratio formula remains simple: divide your loan amount by the property's appraised value. Multiply this result by 100 to get the percentage that represents your LTV ratio. For instance, if you need ₹80 lakhs for a ₹1 crore property, your ratio equals 80%.

Considering the definition of loan to value ratio, the ratio typically stays at or below 80%. The lenders consider it safe. Ratios between 80% to 90% are acceptable but may require additional mortgage insurance coverage. Anything above 90% becomes challenging as lenders view these applications as high-risk investments.

Your creditworthiness plays a role alongside the LTV ratio in determining the loan approval. First-time homebuyers often benefit from special programs that accept higher ratios with conditions.

Your employment history and income stability also influence what ratio lenders will accept. Remember that lower ratios mean better terms, so save more for down payments when possible.

As per the loan to value ratio meaning, imagine purchasing a beautiful home valued at ₹50 lakhs, and you have ₹10 lakhs for a down payment.

Lower ratios often unlock better interest rate options and faster approval processes for borrowers.

Consider Rajesh, who wants to buy a ₹75 lakh apartment in Bangalore for his growing family. He has ₹20 lakhs saved for the down payment, leaving him with a loan requirement. His loan to value ratio becomes approximately 73.33% (which falls within acceptable limits for most lenders). This ratio helps him secure favourable terms, including lower interest rates and reduced processing fees. Rajesh avoided mortgage insurance because his ratio stayed significantly below the 80% threshold.

Also Read About: Mortgage Loans - Interest Rates & Eligibility

Understanding both sides helps you make informed financial decisions about your property purchase.

| Pros | Cons |

|---|---|

| Lower ratios secure better interest rates and terms | Higher ratios require expensive mortgage insurance |

| Helps lenders assess risk and approve instant personal loans faster | This may limit your property purchase options significantly |

| Provides clear guidelines for down payment planning | Changes with property value fluctuations over time |

| Reduces monthly payment burden with lower ratios | High ratios may lead to loan rejection |

| Builds equity in your property from day one | Requires significant upfront cash for low ratios |

Lenders rely heavily on this metric to protect their investments and minimise losses.

Different ratio levels tell distinct stories about your financial position and borrowing capacity.

High LTV Ratios:

Low LTV Ratios:

Reducing your ratio opens doors to better loan terms and significant long-term savings opportunities.

Increasing your down payment significantly reduces the loan amount you need from lenders. Save systematically over several months or years to accumulate a substantial down payment fund. Consider using bonuses, salary increments, or investment returns to boost your down payment capacity.

Selecting a property within your comfortable budget naturally improves your loan to value ratio without additional savings. Research different neighbourhoods to find similar properties at lower prices that meet your requirements. Consider slightly smaller homes or those needing minor renovations to reduce purchase price significantly. Properties in developing areas often offer better value compared to established localities with premium pricing.

Additional principal payments reduce your outstanding loan balance (it automatically improves your current loan to value ratio). Apply tax refunds, work bonuses or unexpected income directly toward your loan principal amount. Consider bi-weekly payment schedules instead of monthly payments to accelerate principal reduction significantly over time.

While the loan to value ratio considers only your primary mortgage amount, the Combined Loan-to-Value includes all debts. CLTV adds second mortgages, home equity loans, and credit lines secured by your property.

| Aspect | LTV | CLTV |

|---|---|---|

| Calculation | Primary mortgage only | All property-secured debts |

| Usage | Initial loan approval | Secondary loan decisions |

| Risk Assessment | Basic risk evaluation | Comprehensive debt analysis |

| Lender Focus | All mortgage lenders | Secondary and equity lenders |

Current market conditions significantly influence acceptable loan to value ratio limits across different lenders and regions. During property booms, lenders often tighten ratio requirements to control risk and prevent defaults.

Economic downturns may see relaxed ratios as lenders compete for qualified borrowers in reduced markets. Interest rate changes affect how lenders calculate acceptable ratios through any loan to value ratio calculator and adjust their lending policies accordingly.

Your loan to value ratio directly impacts your eligibility for various home loan products and terms. Lower ratios increase your chances of approval, while higher ratios may result in rejection. Lenders combine ratio analysis with income assessment and credit history for comprehensive evaluation decisions.

Reserve Bank of India sets specific guidelines for acceptable ratios across different lending institutions.

Also Read About : RBI Guidelines for Loan Recovery

Several key elements determine what ratio lenders will accept for your specific situation.

1. Property Type - Residential properties typically allow significantly higher ratios than commercial or investment properties.

2. Location - Properties in prime locations often qualify for better ratios due to stable value appreciation.

3. Borrower Profile - Your income stability, employment history and existing debts influence acceptable ratio limits considerably.

4. Market Conditions -Current real estate trends and economic conditions affect lender policies and ratio requirements.

5. Lender Policies - Different financial institutions have varying risk appetites and ratio standards for approval decisions.

6. Loan Purpose - Primary residence purchases often get better ratios compared to investment or second home purchases.

Your loan to value ratio serves as a critical factor in securing favourable home loan terms and conditions. Whether you're applying for a home loan or an instant personal loan, lower ratios unlock better opportunities, while higher ratios may increase your borrowing costs significantly throughout the tenure.

Absolutely! Lower loan to value ratio percentages demonstrate reduced lender risk. Lenders reward borrowers who invest more equity upfront with competitive rates and faster approval processes. You also avoid expensive mortgage insurance requirements when ratios stay below the 80% threshold limits.

A 40% loan to value ratio represents an excellent borrowing position with a significant equity investment from your side. Lenders view such applications as favourable, offering their best rates and most flexible terms available. This ratio indicates strong financial planning and substantial down payment capability, which reduces lender risk considerably.

RBI regulations permit a maximum 90% loan to value ratio for home loans up to ₹30 lakhs currently. Loans between ₹30-75 lakhs allow up to 80%, while higher amounts restrict ratios to 75%. Government-backed schemes may offer different limits with specific eligibility criteria and conditions attached.

A 90% loan to value ratio means you're borrowing 90% of property value, requiring only a 10% down payment.

Yes the loan to value ratio directly influences your interest rate, with lower ratios securing better rates consistently. Ratios below 80% typically qualify for lenders' most competitive rates, while higher ratios face premium charges.

Most conventional lenders avoid 100% loan to value ratio financing due to extremely risky exposure concerns. Some government schemes or specialised programs may offer such financing with strict eligibility criteria.

Download our personal loan app to apply for a personal loan. Get up to 2Lakhs* as a personal loan. Download Now!

![]()

Sign into avail a personal loan up to ₹ 2,50,000

Unifinz Capital India Limited is a Non Banking Finance Company (NBFC) registered with the Reserve Bank of India (RBI). lendingplate is the brand name under which the company conducts its lending operations and specialises in meeting customer’s instant financial needs.

RBI CMS

RBI CMS RBI Sachet

RBI Sachet