Did You Know?

We serve loans, the best way you can borrow

If you're thinking about investing in a financial product or obtaining an instant personal loan, it's essential to grasp the various types of interest rate options that are available to you. Typically, there are two prevalent kinds of interest rates – fixed interest rates and floating interest rates. A fixed interest rate stays the same throughout its duration, whereas floating interest rates can change based on several factors, including variable economic or market conditions. In this blog post, we will explore what is a floating interest rate and how it can influence your financial choices.

A floating interest rate means a variable interest rate that may go up or down based on changes in the underlying reference rate or benchmark. The particular reference rate used to determine floating rates is a standard financial index, such as the Repo Rate. The benchmark represents the minimum rate that banks and financial institutions charge to creditworthy borrowers. If the benchmark or reference rate increases, the floating rate will increase, and vice versa.

A fixed interest rate does not change during the life of a loan or financial product, while a variable rate changes in connection with movements in the financial or economic market. You usually find this type of interest rate in personal loans, home loans or some credit card options.

Most importantly, loans with floating interest rates are considered more affordable in the end than fixed-rate loans. And with respect to investments that have variable rates, you can make very predictable and consistent returns over time.

The most common types of floating rate products are credit cards and personal loans. The variable interest rate is charged on unpaid balances. If you read your credit card agreement carefully, you may find something like “This APR will vary with the market.” This means the card’s Annual Percentage Rate (APR) will vary depending on a particular index or benchmark plus a margin.

Another type of floating-rate product is the Adjustable-Rate Mortgage (ARM). It is a kind of home loan where interest rates fluctuate based on spread (a preset margin) and various mortgage indexes, such as the Monthly Treasury Average, the Cost of Funds Index, or SOFR.

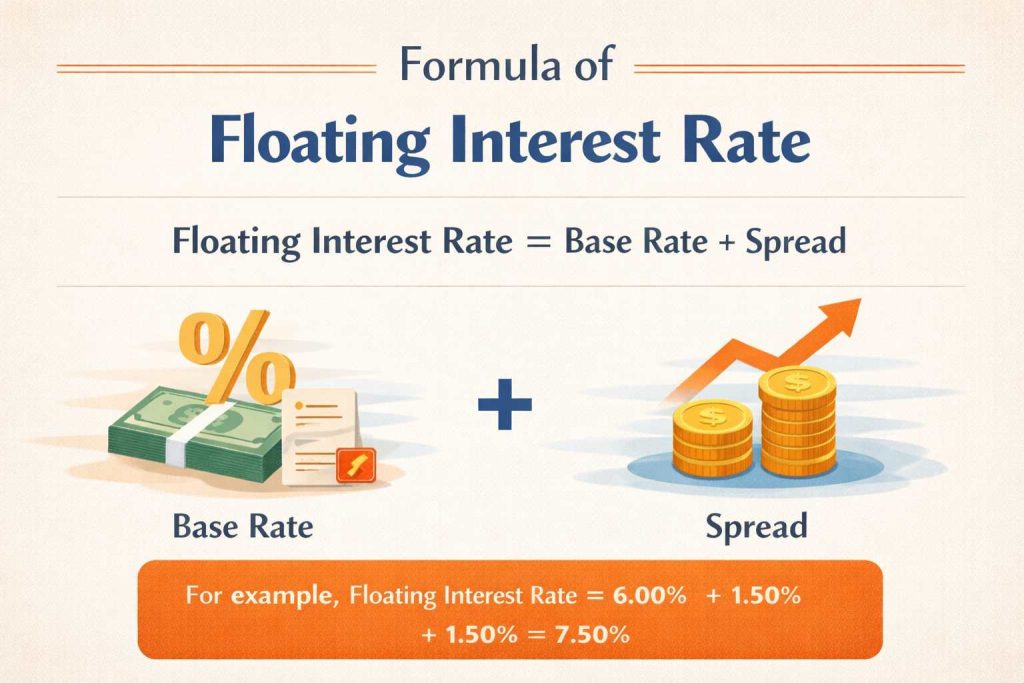

Floating Interest Rate = Base Rate + Spread

Also read: MCLR

The following example will help you better understand what the floating interest rate meaning suggests:

Say you want to take out ₹2,00,000 (P) with a floating personal loan interest rate linked to the RBI’s Repo Rate, which is 6%.

The financial institution offers a spread of 2%.

The loan repayment tenure (N) is determined to be 120 months (10 years).

Using a floating interest rate calculator, we find that:

Effective Interest Rate (R) = Spread + Benchmark Rate

R = 6% + 2% = 8%

Now,

Monthly Value of R = 8% / 12 = 0.67% or 0.0067

Use this value in the floating interest rate EMI calculator to get your Equated Monthly Instalments for the loan:

EMI = [P x R x (1+R)^N] / [(1+R)^N-1]

EMI = [₹2,00,000 x 0.0067 x (1+0.0067)^120 / [1+0.0067)^120-1]

Based on the above floating interest rate example, your monthly EMI amount will be approximately ₹1351.18.

Remember, your EMI will vary based on the current spread and benchmark rate in the market.

If your benchmark changes during the loan tenure, so will the interest rate and hence your EMI.

1. Introductory lower interest rates: Generally, floating interest products offer lower initial rates compared to fixed-rate mortgages and other financial options. This makes them a more attractive option for borrowers and investors who want to reduce their early payments and attain higher returns.

2. Increased Flexibility: Floating interest rates provide investors the opportunity to adjust their financial strategies in line with market changes and current benchmark rates. Borrowers can benefit from possible reductions in interest rates, which can decrease their total borrowing costs.

3. Higher Savings: With floating interest rates, there are always chances of unexpected gains. The investor will yield higher gains if the interest rate declines. On the other hand, the borrower can enjoy greater savings on EMIs when the floating rate on his loan goes down.

4. Better Investment Portfolio: Floating-rate as well as short-term bonds typically perform well when interest rates are going up. Hence, such investment tools are a great option for investors as they help in minimising the volatility of their portfolio and potential risks.

5. Zero Prepayment Penalties: Another benefit is that no prepayment penalties are levied on variable-rate loans and adjustable-rate mortgages. This allows borrowers to pay off their debt early with no additional costs or get the loan refinanced when interest rates are lower.

To better understand the floating rate of interest meaning, it is crucial to evaluate both its benefits and drawbacks. The following are some related risks and constraints.

1. Volatility: While fixed rates are constant, variable interest rates vary with the market, making them nearly impossible to predict. This leads to a difficult task in financial planning, both for the investor and borrower.

2. More expensive in the end: While their interest rate could be lower than a fixed-rate loan initially, this could result in higher total costs for investors and borrowers if rates do rise over time.

3. Limited options available: Not many types of loans and investments come with floating interest rates. This limits your options.

4. Risks of Refinancing: If the rate of interest increases remarkably, it may be difficult to get a floating-rate loan refinanced. In certain cases, you may also need to bear a prepayment penalty in case of refinancing when the interest rates are high.

Also Read: Loan Refinancing

Floating interest rates are commonly used in the banking and finance industry under several circumstances. The examples below will help you understand what is floating interest rate and how it is used:

1. Many credit card companies offer a variable rate of interest. The interest charged here is typically the prime rate and a certain spread.

2. A common use of floating interest rates is in mortgage loans. Banks and financial institutions follow the current index or reference rate, and the interest is calculated as = prime rate + 1%.

3. It is also common for large corporate clients to take out variable-rate loans. The total interest rate is determined by adding (rarely subtracting) the stated base rate to a margin or spread.

There are several factors impacting your floating interest rates. Discussed here are some of the common economic factors:

1. RBI’s Monetary Policies

2. The Current Repo Rate

3. Fiscal Deficit

4. Inflation Rate

5. Global and Foreign Interest Rates

The variable interest rate is subject to fluctuations due to the performance of the economy and market changes. Therefore, using a floating interest rate calculator can help determine your interest rate and EMI.

Also read: Factors Affecting Interest Rates

| Basis | Floating Interest Rate | Fixed Interest Rate |

|---|---|---|

| Interest Rate | The rate of interest tends to fluctuate throughout the loan period or investment tenure. | The interest rate remains fixed. |

| Impact | As the interest rate goes up or down, the EMI amount will also change, as well as the return on investment. | The EMI amount remains constant during the entire duration of the loan. |

| Predictability | The good thing about variable interest rates is that they often start lower— only to go up over time once they adjust to market conditions. | By choosing fixed-rate loans or investments, you can have a definite awareness of your EMIs and the returns throughout the term. |

| Initial Interest Rates | The floating interest rates start lower initially, but may increase over time. | The fixed rates start higher because they offer more stability and predictability. |

| Prepayment Penalties | They do not carry any prepayment charges in most cases. | Prepayment penalties are applicable if you want to repay the loan before the end of its term. |

| Risks | A variable-rate loan or investment carries more risk. | It is less risky because the rates are fixed and offer more certainty. |

A floating interest rate is suitable if you have a high risk appetite and think that the base rate will decrease or stay the same over time. In these situations, you might prefer a lower interest payment or maintain the same rate throughout the duration of the loan.

There are various factors that could affect your choice between a floating and a fixed interest rate. Let’s understand here.

1. Market Conditions: It is essential to stay vigilant of how interest rates are changing with fluctuating market conditions. If the rates tend to go up, you can have steady payments with a fixed-rate loan or investment. On the other hand, go for a floating rate if you are expecting the rates to drop or stay low in the future. Analysing the past interest rate trends and market conditions can help you decide.

2. Risk Appetite: If you do not prefer surprises and want steady payments, a fixed rate of interest is for you. However, if you have good risk tolerance, go for a floating rate.

3. Loan Duration: Fixed interest rates are best for long-term loans because they provide you with stability in the long run. Short-term loans and investments, however, are much less rate sensitive and floating rates make a lot of sense.

4. Prepayment Regulations: Various fixed-rate loans impose a penalty for early repayment. In contrast, floating-rate loans often offer more flexibility regarding prepayment rules.

The choice between a floating or fixed interest rate is completely up to you, your money goals, financial stability and risk appetite.

Knowing the floating interest rate meaning and how it is calculated can prove to be beneficial if you are considering different credit choices or investments. Evaluating the advantages and disadvantages of a floating interest rate ensures that you can get the best returns out of your investments or handle your debts efficiently. Whether to choose a fixed or variable interest rate for an individual loan or an instant personal loan will come down to market conditions, financial objectives, and the risk capacity of the applicant.

A floating interest rate means that the interest rate may vary depending on the economic and market conditions. Say, you have a loan which carries variable interest rates linked to the change in the Repo Rate. Your interest rate will move up or down with every movement in the Repo Rate.

Variable rates of interest can change with the fluctuating prime rate or market situations. Therefore, your EMI will change from time to time over the loan tenure. The rates, to start with, can be lower, but they vary gradually as per market conditions. In contrast, a fixed interest rate remains the same over the term of your loan. This leads to fixed EMI payments and more certainty.

Interest rates on floating-rate loans usually fluctuate according to an index or a different benchmark interest rate. Additional factors that can influence these rates include the monetary policy set by the government, inflation levels, and the fiscal deficit.

Floating interest rates usually begin at a lower level, enabling you to reduce your borrowing costs. Although the rate may increase later on, it is likely to decrease again due to its volatile nature.

One of the limitations of a floating interest rate is that your EMIs may increase when the market rate goes up and your interest rate rises.

Since a floating interest rate depends on market conditions and a benchmark rate, it involves a certain amount of risk of increased EMIs, uncertainty, and higher overall costs. On the flip side, you can enjoy greater savings when the interest rate drops, and so are your EMIs.

A floating interest rate is suitable if you have a good risk tolerance or if you are ready to bear the fluctuations in interest payments or EMIs.

No, floating interest rates may also be available on certain credit card options and personal loans.

A floating interest rate typically changes every quarter.

Yes, most banks and financial institutions give you the option to switch from a floating to a fixed interest rate, and vice versa.

Download our personal loan app to apply for a personal loan. Get up to 2Lakhs* as a personal loan. Download Now!

![]()

Sign into avail a personal loan up to ₹ 2,50,000

Unifinz Capital India Limited is a Non Banking Finance Company (NBFC) registered with the Reserve Bank of India (RBI). lendingplate is the brand name under which the company conducts its lending operations and specialises in meeting customer’s instant financial needs.

RBI CMS

RBI CMS RBI Sachet

RBI Sachet